The recent dramas of Britain”s Royal Family highlight the momentous step families may sometime face in cutting someone out of their inheritance. Rules on such matters differ across the US. The author – a regular contributor – considers the issues.

The lives of famous people excite prurient curiosity

with their divorces, family disputes and dramas regularly

appearing in the media. The recent decision by the UK’s King

Charles lll to remove the titles of his brother, Andrew – no

longer a prince – is a particularly dramatic case. Beyond the

immediate issues that this story creates, however, it reaises

questions about what “disinheritance” means for families, and how

this applies in countries such as the US.

The author here is familiar FWR contributor Matthew Erskine,

who is also a member of this news service’s editorial board. The

editors here are pleased to share these views; the usual

editorial disclaimers apply. To comment, email tom.burroughes@wealthbriefing.com

and amanda.cheesley@clearviewpublishing.com

King Charles III’s recent decision to strip Prince Andrew of his

royal titles and evict him from his residence has captured global

attention, but it also highlights a reality many families face

but without the royal drama: the complex process of

disinheritance.

Whether you’re a business owner protecting decades of hard work

or a parent navigating difficult family dynamics, understanding

how to properly exclude someone from your estate is crucial

– and far more complicated than simply leaving them out of

your will.

The business case for strategic

disinheritance

In most states, a parent or testator generally has full legal

power to disinherit an adult child, provided the intent is clear

and unambiguous in their will or trust instrument. This power

extends beyond parent-child relationships to any potential heir,

making it a valuable tool for business owners, entrepreneurs, and

high net worth individuals who need to protect their legacy.

But here’s the critical point most people miss: A simple omission

isn’t enough. The will must specifically identify the child to be

excluded and should state that the omission is intentional, not

accidental. This requirement exists because courts assume family

members were accidentally forgotten rather than deliberately

excluded.

The legal safeguards you must navigate

1. Protecting children born after your will

Most states include robust protections for “omitted children”

– those born or adopted after you execute your will. If a

testator did not have living children when signing the will, an

after-born or after-adopted child is generally entitled to a

statutory share that mirrors what they would receive under

intestacy, unless the will leaves “all or substantially all” the

estate to the child’s other parent, and that parent survives and

takes under the will.

This creates a particular challenge for entrepreneurs and

business owners who may start families later in life or through

blended family arrangements. If the testator had living children

and made gifts to them, the omitted child receives a proportional

share based on what the living children receive, drawn first from

the residue and then equally from devises to other beneficiaries.

2. The surviving spouse exception

Here is where most state laws draw a hard line: most states do

not allow a testator to completely disinherit a surviving spouse.

Regardless of what the will states, the spouse may elect to take

against the will and receive a “statutory forced share.”

The financial implications are significant. Typically, if the

decedent leaves issue (children or grandchildren), the spouse is

guaranteed a minimum amount outright plus a life interest in a

portion of the remaining estate. The exact percentages and

amounts vary by state, but the principle remains consistent:

surviving spouses have protected rights that cannot be

circumvented through disinheritance.

What makes this particularly challenging for business owners is

that this share may include some non-probate assets, such as

those held in revocable trusts, making careful planning essential

to avoid unintended inclusion. Your carefully structured business

succession plan could be disrupted if you haven’t properly

accounted for spousal rights.

3. Community property states: A different playing

field

If you live in a community property state (Arizona, California,

Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, or

Wisconsin), the rules change dramatically. In these

jurisdictions, each spouse automatically owns a 50 per cent

interest in all property acquired during the marriage, regardless

of whose name is on the title.

This fundamental difference means that disinheritance strategies

must account for the fact that a surviving spouse already owns

half of the marital estate by law.

You can only disinherit someone from property acquired outside of

the marriage and your half of the community property. Attempting

to dispose of your spouse’s community property interest through

your will is not only ineffective, but it can also trigger costly

litigation and family disputes.

Community property states also have different rules regarding

what constitutes separate versus marital property, and some allow

couples to convert community property to separate property (or

vice versa) through written agreements. For business owners in

community property states, this creates both challenges and

opportunities for estate planning that do not exist in common law

property states.

Best practices for bulletproof disinheritance

1. Express your intent clearly

Always expressly state the desire to disinherit an individual;

ambiguity risks statutory intervention. Your will should include

language such as: “I intentionally make no provision for my son

John Doe, and this omission is deliberate and not accidental.”

2. Use multiple tools in combination

Consider using a combination of wills, trusts, and updated

beneficiary designations for thorough implementation. Trusts are

highly effective tools for controlling distributions and

safeguarding from future litigation, especially in complex family

structures or where privacy and asset protection are paramount.

Don’t forget the often-overlooked details: All beneficiary

designations on accounts (insurance, retirement, bank) should

also be reviewed and updated to avoid accidental inheritance.

3. Understand the limitations

Be aware of protections for omitted children and forced-share

rights for surviving spouses – they cannot be circumvented

by omission alone. This is where many DIY estate plans fail,

costing families thousands in litigation and potentially

undermining your intent entirely.

4. Work with experienced counsel

Discuss your intentions with your estate attorney to tailor

strategies, especially in unique family arrangements or

high-value collections. The stakes are too high for generic

online templates when you’re dealing with substantial assets or

complex family dynamics.

The bottom line

King Charles’s formal and public action serves as reminder:

whether royal or ordinary, for a disinheritance to stand, the

process must be as intentional and as well-documented as the

reasoning behind it.

For business owners and high net worth individuals, the lesson is

clear: protecting your legacy requires more than just financial

acumen – it demands legal precision. The difference between

a successful disinheritance and a costly family lawsuit often

comes down to the quality of your planning and the clarity of

your documentation.

Whether you are protecting a family business from a spendthrift

heir or ensuring that your philanthropic vision survives family

disputes, the key is acting deliberately and working with

qualified professionals who understand both the legal

requirements and the family dynamics at play. In estate planning,

as in business, the details matter – and getting them wrong

can be expensive.

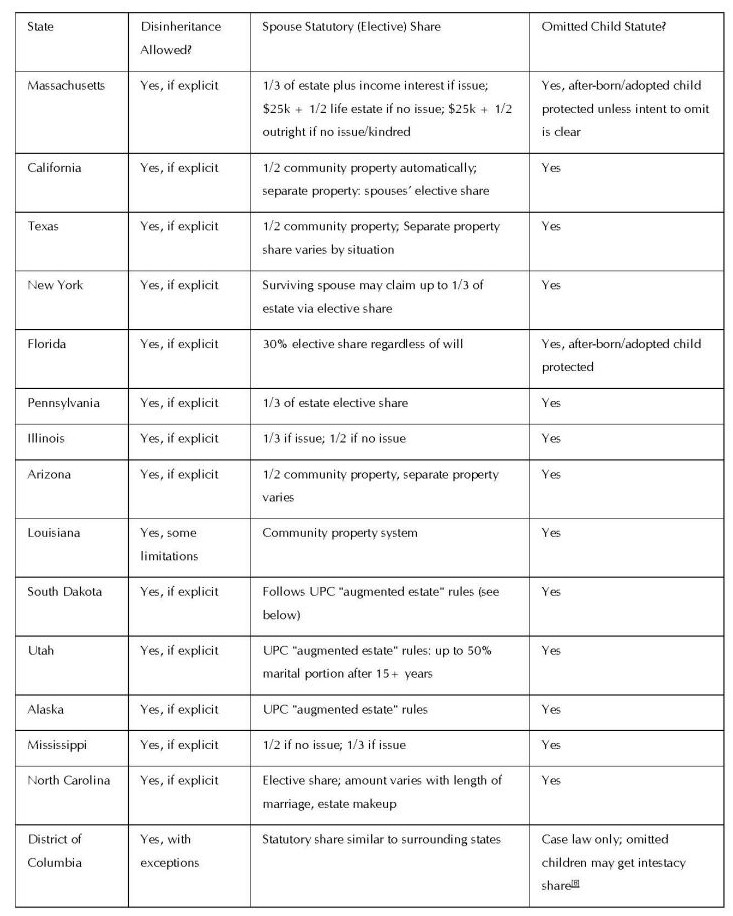

Below is a summary table outlining each state’s approach to

disinheritance and statutory share (elective share) for surviving

spouses. Most states allow adults to disinherit children if

stated explicitly in estate documents, but minor children and

spouses are almost universally protected.

Elective spouse shares and omitted child statutes vary widely by

jurisdiction.

— Community property states (Arizona, California, Idaho,

Louisiana, Nevada, New Mexico, Texas, Washington, Wisconsin)

automatically give half of marital property to the surviving

spouse, regardless of what the will says.

— Uniform Probate Code (UPC) states (e.g., Alaska,

Colorado, Hawaii, Kansas, Minnesota, Montana, North Dakota, South

Dakota, Utah, West Virginia) use the “augmented estate,” which

blends probate and non-probate assets to calculate the elective

share, generally 50 per cent of the marital portion based on

years married.

— All states include omitted child statutes, protecting children

born or adopted after a will is written unless the omission is

intentional or the child is provided for outside the will.

— Where a statutory spouse share exists, surviving spouses must

proactively elect within time limits (usually six to nine months

post-probate).